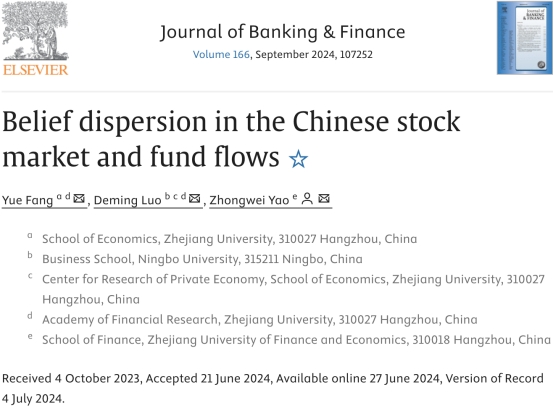

近日,我院姚钟玮博士作为通讯作者,与浙江大学经济学院百人计划研究员方岳、宁波大学商学院教授罗德明的合作论文“Belief dispersion in the Chinese stock market and fund flows”于金融学领域权威学术期刊、ABS 3星期刊、我校认定的外文1级A期刊Journal of Banking & Finance上正式发表。

Abstract

This study explores how Chinese mutual fund managers’ degrees of disagreement (DOD) on stock market returns affect investor capital allocation decisions using a novel text-based measure of expectations in fund disclosures. In the time series, the DOD negatively predicts market returns. Cross-sectional results show that investors correctly perceive the DOD as an overpricing signal and discount fund performance accordingly. Flow-performance sensitivity (FPS) is diminished during high dispersion periods. The effect is stronger for outperforming funds and funds with substantial investments in bubble and high-beta stocks, but weaker for skilled funds. We also discuss the financial sophistication of investors and provide evidence that our results are not contingent upon such sophistication.

摘要

本文基于中国公募基金定期报告,构建了一个新颖的基于文本的专业投资者股票市场预测分歧指标,研究个人投资者的投资决策如何受到专业投资者的影响。时序结果显示,基金经理股市预测分歧能够显著负向预测未来股票市场收益率。截面结果表明,基金投资者能够正确将基金经理间的预测分歧解读为市场被高估的信号,从而给予基金业绩相应地折扣。在预测分歧较高时期,基金流量-业绩敏感性降低,且该效应在业绩优异和大量持有泡沫股票和高系统性风险股票的基金子样本中更显著,但投资能力较强的基金经理可以缓解这一情况。本文还讨论了基金投资者是否具备复杂学习能力,并提供证明表明文章的结论并不依赖这一假设。

姚钟玮博士的主要研究方向为:共同基金、投资者行为和实证公司金融。研究成果发表在Journal of Corporate Finance, Journal of Banking & Finance, Pacific-Basin Finance Journal上。